Spawn AI Agents that

discover alpha

Momentum Sentinel

Seek intraday breakout alpha across NIFTY 50 high-beta names

Sharpe

Wakes

Findings

P&L

Sharpe

Wakes

Findings

Agent P&L

Strategy Performance

Strategy Return

+15.3%

Benchmark

+6.3%

Sharpe Ratio

1.96

Max Drawdown

-4.1%

Smart Growth

12,847+

Strategies backtested on the platform, building research depth and reaching performance benchmarks.

1.2B

Data points analyzed across equities, derivatives, and indices for comprehensive research coverage.

+23.5%

Average annual return improvement across diversified strategies, balancing risk while steadily increasing growth.

1,800+

Stocks available to backtest across NSE and BSE, from leading indices to mid & small cap universe.

Your research stack is bleeding ₹.

By the time you’ve finished researching across seven tools, the move’s already happened. The setup ran without you.

Your current stack

- ₹2,100/mo

TradingView

Premium

- ₹800/mo

Sensibull

Pro

- ₹999/mo

Opstra / DefineEdge

Positional

- ₹333/mo

screener.in

Premium

- ₹650/mo

Trendlyne

DVM Pro

- ₹500/mo

StockEdge

Premium

- ₹1,700/mo

ChatGPT / Claude

Pro

What it’s costing you

- Seven tabs open before the 9:15 bell even rings.

- 2+ hours of prep for a single intraday idea.

- Copy-pasting charts into ChatGPT for answers it can’t verify on Indian data.

- ₹7,000+/month in subscriptions before you place one trade.

- 5+ sources manually re-checked before every entry.

- No second pass, your thesis goes unchallenged into the open.

- Tools that never talk to each other. You are the integration layer.

alphabench

- 1,800+ NSE & BSE equities and live F&O chains, one unified agent.

- Cross-synthesis finds confluences across price, flow, and fundamentals you’d miss.

- 2 hours → 12 minutes. Cut pre-market research time by ~10x.

- Frontier AI models (Claude, GPT, Gemini) doing the heavy lifting on your watchlist.

- Exact setups confirmed or denied with a deterministic RaptorBT backtest, no hallucinated edge.

- alphabench alerts, ambient agents running your strategies through every session, 24/7.

- Build your own alerts in plain English, scheduled around the IST trading day.

One agent. Every Indian market source. Synthesized.

alphabench fans out across data, lets frontier models reason over it, runs the numbers in RaptorBT, and emails you the moment a setup fires, through every session.

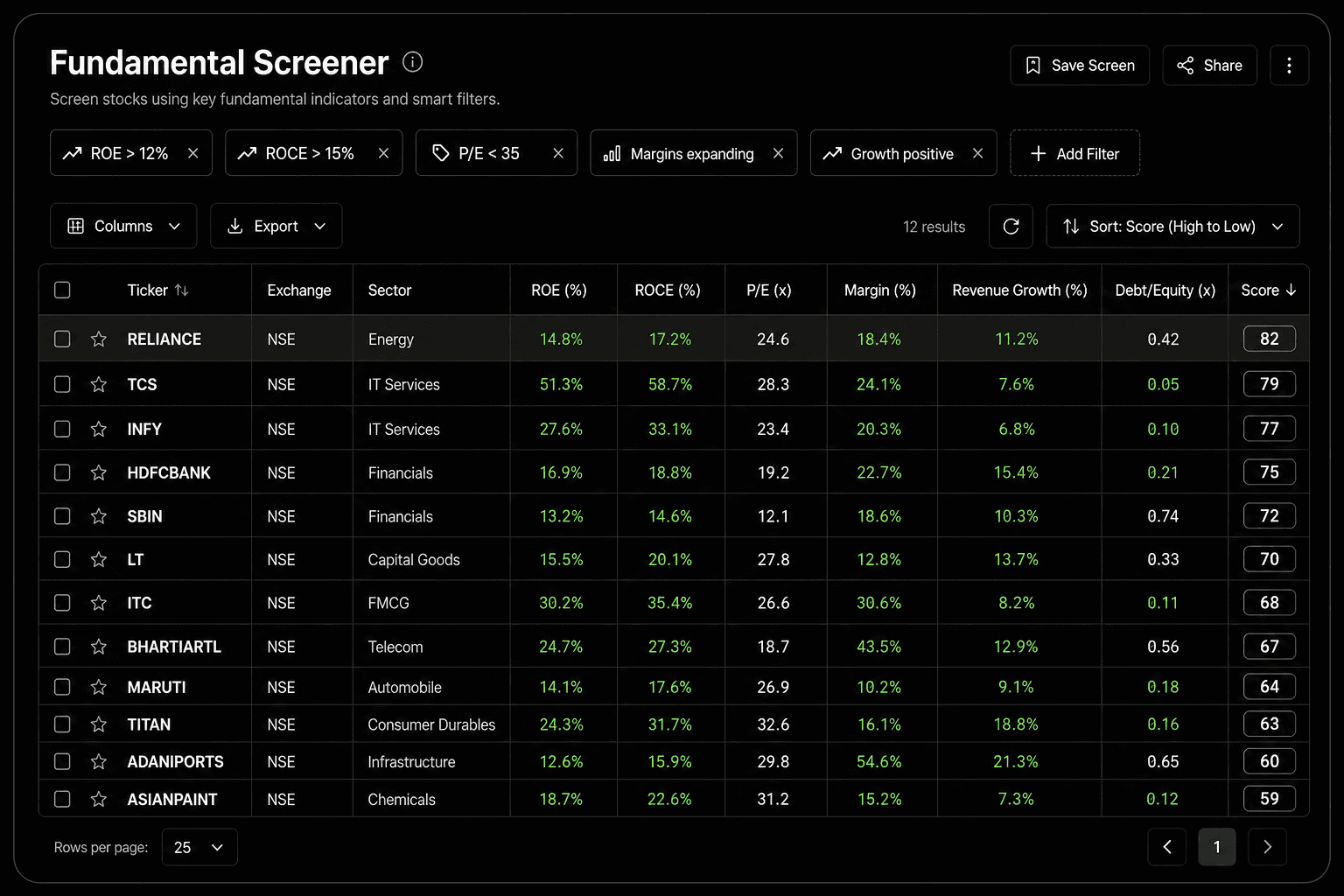

Screen 1,800+ NSE & BSE names

30+ fundamental factors, ROE, ROCE, P/E, margins, growth.

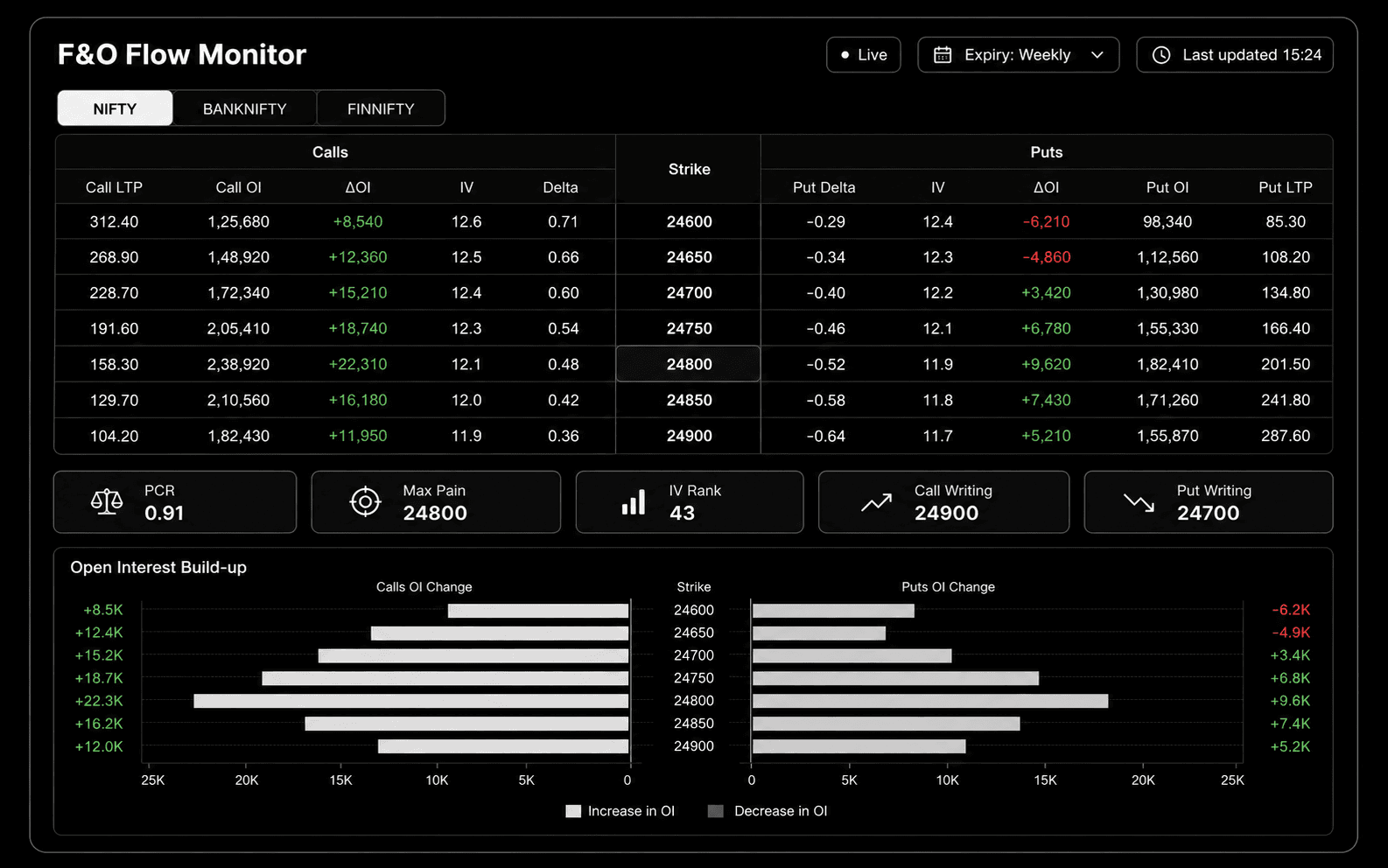

F&O flow & open interest

NIFTY · BANKNIFTY · FINNIFTY option chains, OI build-up, PCR.

Live news & sentiment

Corporate actions, results, RBI & SEBI headlines, X chatter.

10+ years of price history

1-minute to daily candles across equities, futures & options.

Frontier AI models synthesizing

Cross-references flow, fundamentals & price action into one thesis.

Pre-market brief

Overnight cues, SGX/GIFT NIFTY, ADRs, top gappers, key events at 9:15.

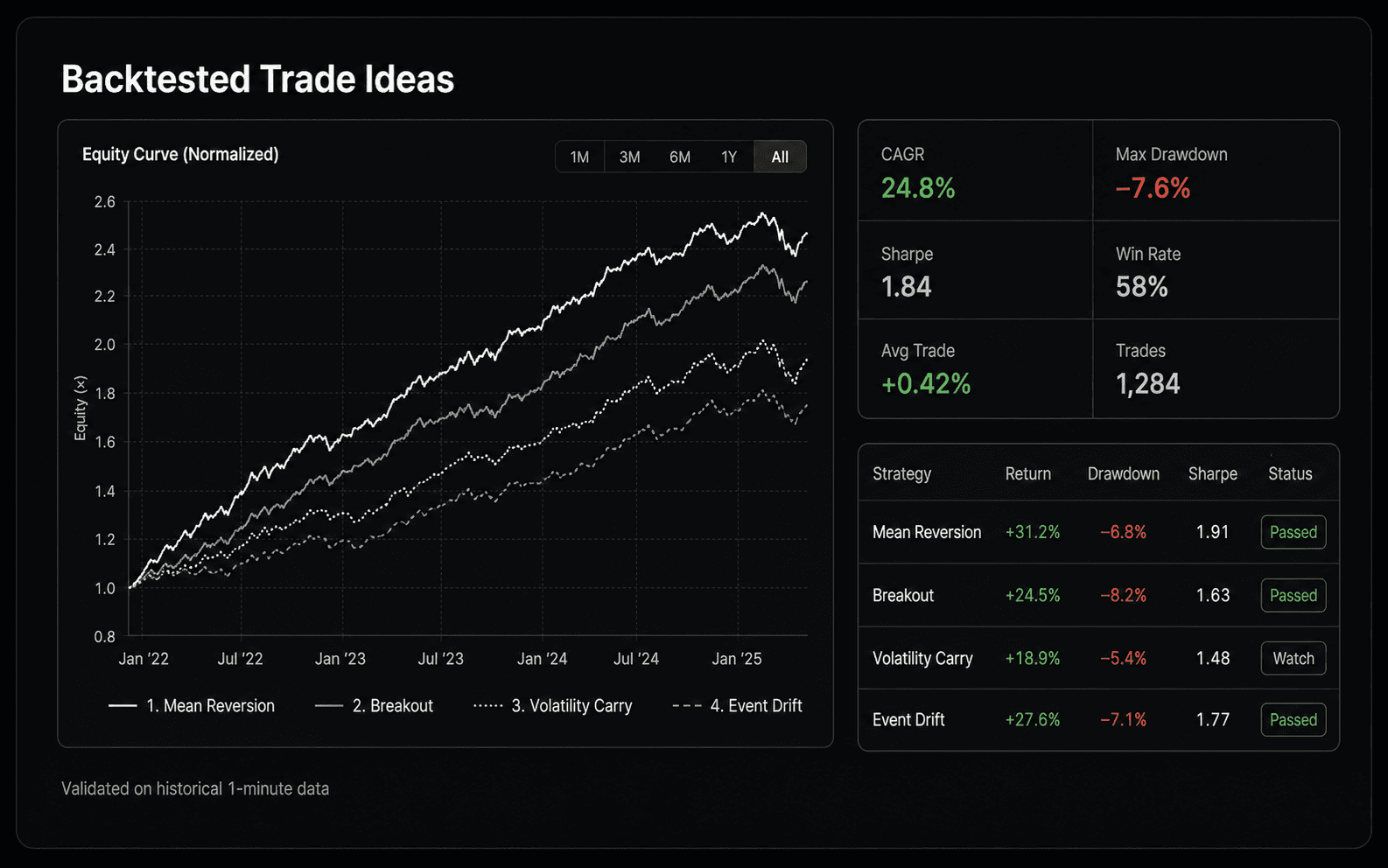

Backtested trade ideas

Every setup confirmed on real history by RaptorBT before it reaches you.

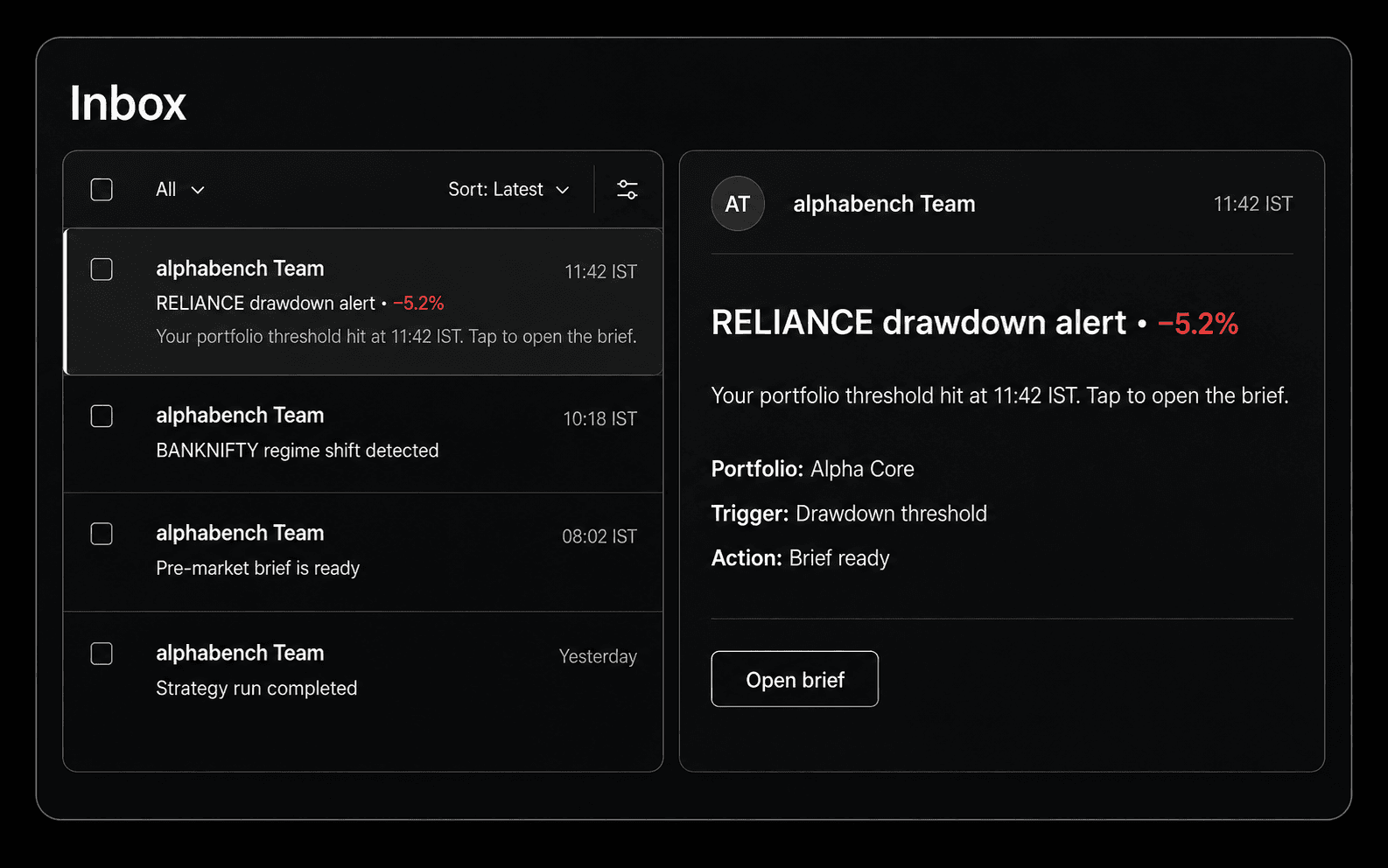

Portfolio & strategy alerts

Drawdown, regime shift, and signal triggers on your deployed agents.

Emails you the moment it hits · 24/7

Your portfolio threshold hit at 11:42 IST. Tap to open the brief.

Built for every level.

alphabench meets you where you are. Where are you on your trading journey?

Ask alphabench for a trade idea or a plain-English explanation of any market concept, “What’s a CPR bounce on NIFTY?”

It plans across 1,800+ names and F&O chains, writes the strategy, and runs a real backtest on RaptorBT, live.

You get a clean dashboard, equity curve, Sharpe, drawdown, win-rate, and a clear answer in INR terms.

Turn the answer into an alert. alphabench reruns it on the IST schedule and emails you the moment it fires.

Smarter Research With AI Forecasts, Institutional Analytics, and Real-Time Data

Describe your strategy in plain English and get backtests within seconds, with zero unnecessary complexity.

RaptorBT is open-source, battle-tested, and blazing fast. Institutional-grade calculations with full transparency.

Get AI-powered regime detection, parameter sensitivity analysis, and Monte Carlo simulations to maximize long-term edge.

Sample Strategies

15min ORB

Sharpe

2.24

Max DD

-3.2%

Win Rate

64.2%

VWAP Scalp 5m

Sharpe

1.89

Max DD

-2.8%

Win Rate

58.6%

CPR Bounce

Sharpe

2.05

Max DD

-4.1%

Win Rate

61.3%

Momentum 5m

Sharpe

1.73

Max DD

-3.5%

Win Rate

55.9%

Supertrend 5m

Sharpe

1.91

Max DD

-5.7%

Win Rate

52.4%

| Name | Return | Sharpe | Max DD | Win Rate |

|---|---|---|---|---|

| 15min ORB | +18.7% | 2.24 | -3.2% | 64.2% |

| VWAP Scalp 5m | +12.3% | 1.89 | -2.8% | 58.6% |

| CPR Bounce | +16.1% | 2.05 | -4.1% | 61.3% |

| Momentum 5m | +14.8% | 1.73 | -3.5% | 55.9% |

| Supertrend 5m | +21.2% | 1.91 | -5.7% | 52.4% |

Need Help

Common questions about the platform, data coverage, and getting started with AI-powered quant research.

An AI agent is a specialized LLM with a focused tool surface. alphabench spawns four core agents: Planner (orchestration), Quant (backtest execution), Researcher (data discovery and fundamental screening), and Diagnostician (trade forensics). They collaborate to handle your request, share message history, and each agent only sees the tools it owns, which keeps reasoning sharp and answers truthful.

The Planner agent reads your message and routes work. A backtest request goes to the Quant agent. A "find me stocks with ROE > 18" request goes to the Researcher. A "why did this strategy lose money" request goes to the Diagnostician. Most prompts use two or three agents in sequence, and you see one coherent answer.

Describe your strategy in plain English. The Planner agent interprets it, the Quant agent translates it into a strategy DSL and calls RaptorBT (our open-source Rust engine), which runs the backtest deterministically and returns equity curves, trade logs, and metrics. No LLM is in the execution path, so backtests are reproducible.

The Quant agent handles any intraday strategy: Opening Range Breakouts (ORB), CPR levels, VWAP scalping, momentum breakouts, options straddles, futures trending. Use 1-minute to 15-minute timeframes with time-of-day filters, session-based exits, and real slippage modeling.

1,800+ NSE & BSE equities with 10+ years of daily data, active F&O instruments, weekly and monthly options chains, and 30+ fundamental fields per equity (ROE, ROCE, P/E, P/B, revenue growth, margins). Intraday data goes down to 1-minute candles. The Researcher agent has read-only access; the Quant agent uses the same data to backtest.

Yes. The Quant agent supports straddles, strangles, spreads, iron condors, calendar spreads, diagonals, and custom multi-leg strategies on NIFTY and BANKNIFTY with real historical options chain data and per-leg expiry control.

Yes. Paper trade with tick-level live simulation first, then deploy to live trading with Zerodha integration. Monitor P&L, positions, and signals in real-time via WebSocket updates. Strategy health monitoring runs as a separate agent loop after deployment.

Yes. You can start for free with no credit card required. The free tier includes generous daily backtest limits and full access to equity data.

Ready to Find Your Edge?

We're scaling our services. Request access and we'll notify you as soon as possible.

alphabench